Taking loans to cover payments (debt danger sign #2)

A danger sign of a debt problem is borrowing money before payday...

Back in 2013 the payday loan market was booming. Chirpy jingles and TV puppets were advertising quick cash solutions to get you through those last few days before payday.

Many people saw this type of loan as a quick and easy way to get cash for unexpected expenses. The trouble was, this type of high-cost short-term credit often caused more money problems than they solved.

Clients contacting us for help with multiple payday loan debts were common. There were inadequate credit checks and affordability checks. Payday loans were being rolled over. Eye-watering interest rates were charged (often well over 1,000% APR), then there were often hefty fees and charges increasing the total repayment amount. People were taking out new payday loans to pay off existing payday loans.

Something had to be done.

In 2015, new rules were introduced by the Financial Conduct Authority (FCA) in an attempt to make the payday loan market fairer for borrowers by offering more responsible lending. Payday loan companies were told to improve their affordability checks, to make sure the people they were lending to would be able to pay their loan back. Loan repayment details, costs, terms and conditions needed to be made clearer. And finally, a cap on fees and rollovers was introduced.

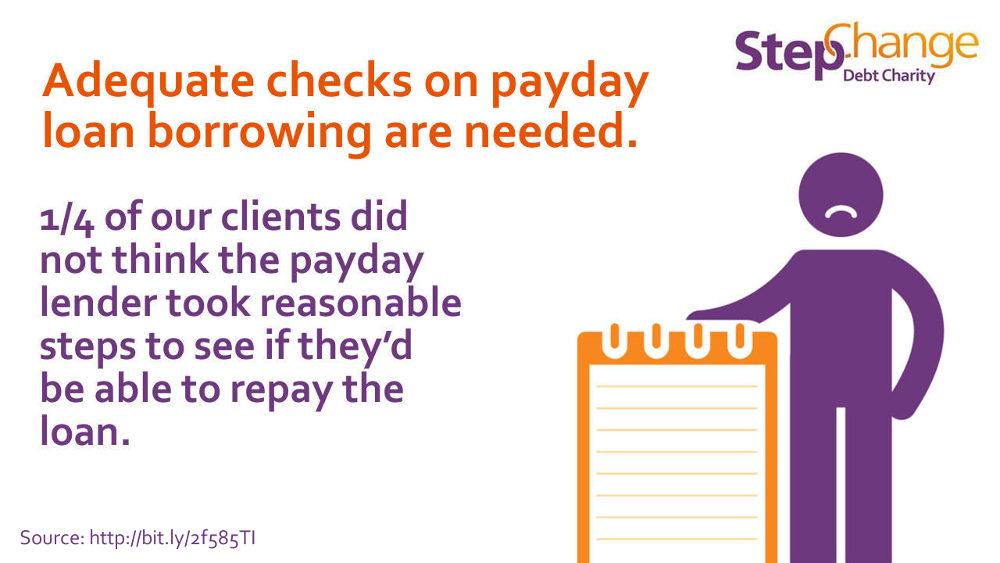

It’s nearly two years since the rules were introduced and we wanted to see if they’d made a difference to the payday loan market.

We talked to clients who’d taken out payday loans after the new FCA rules were in place, to find out how they’d been treated.

From talking with our clients we found out:

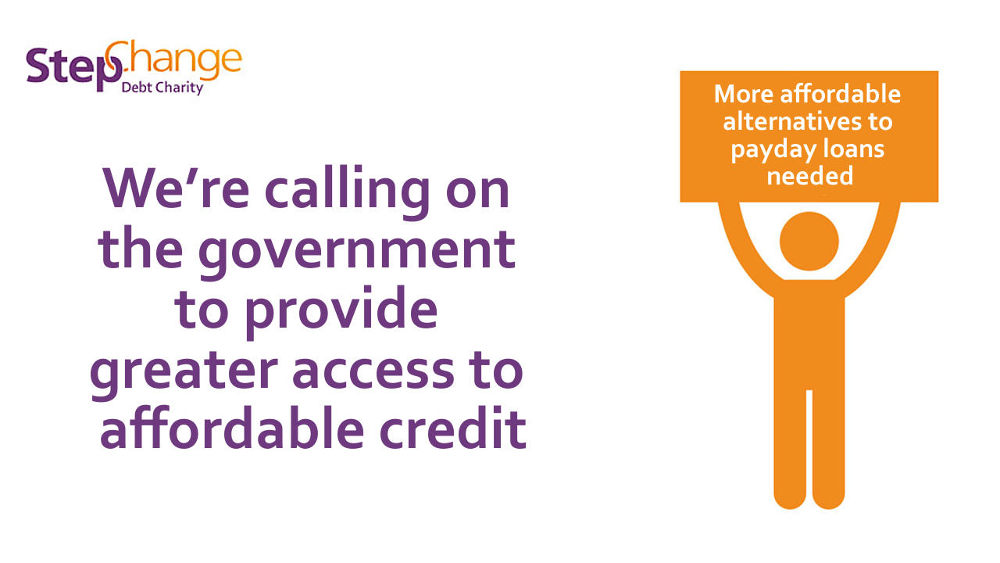

We’ve seen a reduction in the number of people coming to us for help with these types of loans. However, this doesn’t address the issue that some people still need access to affordable credit. In fact, of those we spoke to that had been rejected, we found that:

It’s clear that stronger regulations are needed to ensure the market is fair for consumers. However, introducing rules to regulate the market doesn’t reduce the need for credit in the first place.

That’s why we’re calling for stronger action from the FCA on payday loans and for the government to provide better access to affordable credit.

Our latest report, Payday loans: The next generation, investigates the ways the FCA could continue to improve the market.

If you need some extra cash it can be very tempting to take out a payday loan as a quick solution. However, this may not always be the best option and it’s good to know the alternatives to payday loans that could help.

If you’re struggling with payday loan debts then you should contact us for free and impartial debt advice.