We ask…how do you survive the longest month of the year?

January can feel like the longest month of the year: Christmas is...

Much like an illness, you can tell if you have a debt problem based on the symptoms that can arise. We call these symptoms ‘debt danger signs’.

Much like an illness, you can tell if you have a debt problem based on the symptoms that can arise. We call these symptoms ‘debt danger signs’.

As part of Debt Awareness Week we’re discussing the five danger signs to help you avoid them, or if you’ve tried to deal with your finances in this way, how to get help sooner.

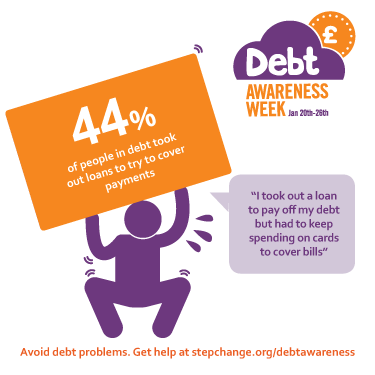

One of the danger signs of a debt problem is borrowing money before payday to cover everyday things, like bills, food or travel.

It may seem like a quick fix but taking loans to cover things you pay regularly will only make the situation worse.

What’s wrong with borrowing money to cover bills or living costs if you’re a bit short? You’re just a slider away from a cash boost. Well the answer is that taking more debt isn’t a problem; it’s the result of the problem.

If you can’t pay all of your essentials without contacting the bank, searching for a short-term loan or asking a mate for a sub, you need to confront the elephant in the room and admit your budget is stretched too far.

It’s not just us saying taking loans is a danger sign of a debt problem. The very people we help on a daily basis tell us so. We asked our clients about the moment they realised they had a debt problem; here’s what they said:

“I maxed out all the credit cards and still didn’t have enough to survive the month”

“A household bill direct debit got returned just after payday. I’d already tried to extend the overdraft and get additional loans but they were rejected. We were paying massive fees on unauthorised overdrafts. The phone calls and letters were constant. I knew I needed to do something or we’d lose our home.”

If you’re struggling, getting a short-term loan is probably not the answer. Picture this: you’re sat at your kitchen table with a pile of bills your pay won’t stretch to cover. You do a quick search online, click, click, click, you find a nice friendly site that is more than happy to lend you the money. Phew! Cash wings its way into your bank account and the problem is solved…Right?

What the adverts don’t show is what happens in the following weeks. You have the same wage, same bills but you’re minus the loan repayment that comes out the bank on payday. How do you get through that month? You borrow more. You’re now trapped in a cycle of payday loan borrowing.

If you’re worried, the very best thing you can do is look at your spending. It may be that just by looking at your budget and cutting back a bit you can get yourself back on track. Or you may have stretched your budget as far as it will go and you need some free, impartial debt advice.

The key to finding out why you’re relying on loans to survive is to take a good look at your situation. Follow this simple checklist:

Hopefully you’ll recognise that taking loans to cover basic payments is not a solution but a danger sign of a debt problem. All week StepChange Debt Charity are talking about recognising those danger signs.

In seconds the StepChange Debt Danger Signs test can tell you how many apply to you, how to avoid the others, and how we can help with free and impartial debt advice.

Client quotes obtained in debt danger signs survey, Dec 2013.