10 ways to treat mum this Mother’s Day

Mum, mam, mother, ma. Whatever you call her, you don’t need to...

This page contains information about debt solutions available in England, Wales and Northern Ireland. Debt advice in Scotland involves similar but different solutions. If you are considering an IVA as a debt solution, please ensure that you fully understand the risks involved when entering an IVA.

The rules for using credit on an IVA are very strict – and quite confusing! When go on an IVA, credit card and loan warnings will be issued by your IVA provider, but what about other forms of credit? Find out more.

Are these “credit”?

We all know that as part of the terms and conditions of your IVA proposal you should avoid taking out further credit.

We’d discourage any form of borrowing at all, but you can borrow less than £500 without your supervisor’s permission in writing.

But what is meant by “credit”? Let’s investigate…

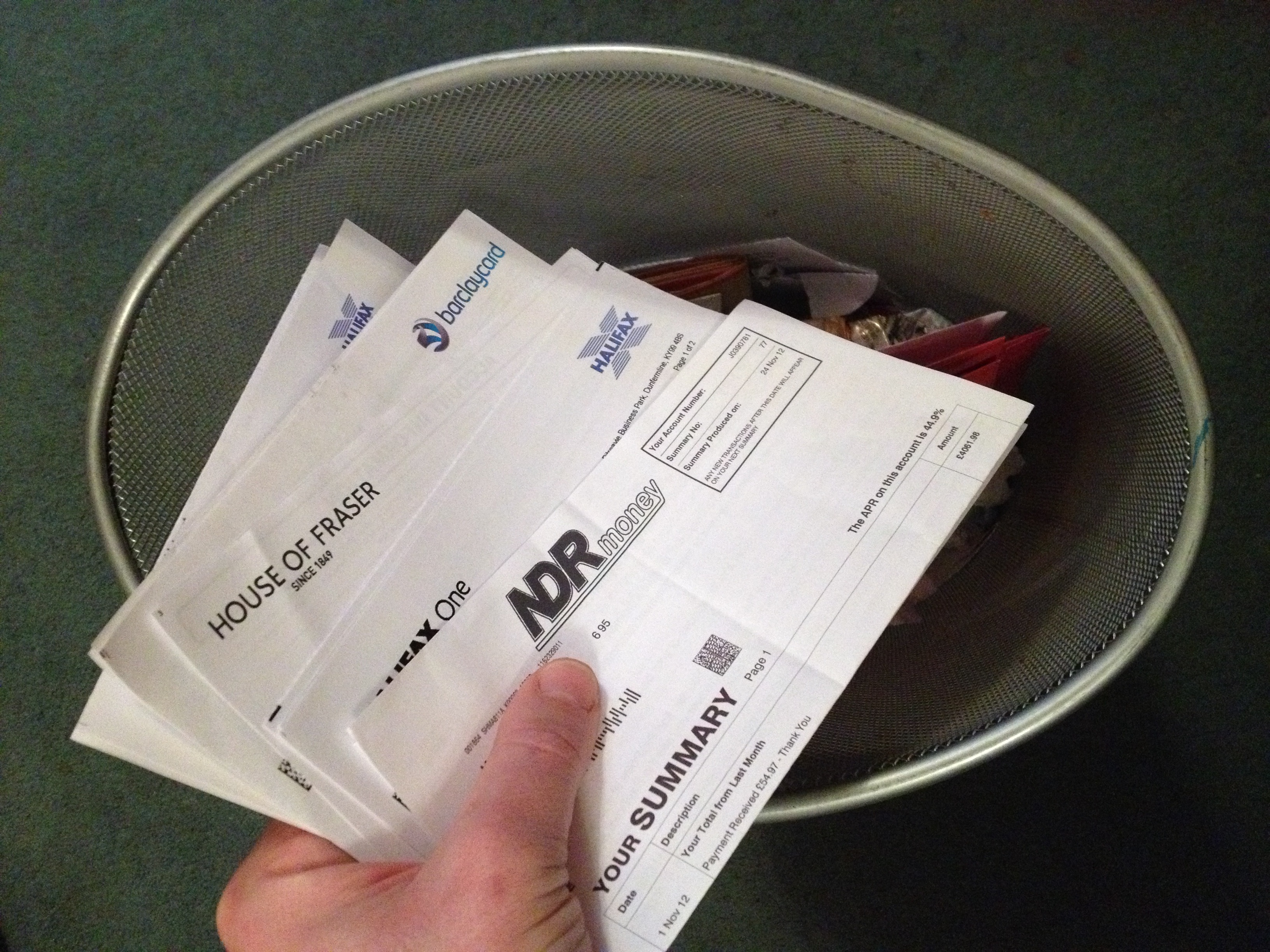

The credit you’re not allowed to take out include credit cards, store cards, loans, payday loans, guarantor loans or any consumer credit act debts.

These are against the terms and conditions of your IVA and frankly, they defeat the purpose of your IVA.

Quick recap: On an IVA, a loan (guarantor or payday), credit card, store cards – and any consumer credit is completely out of bounds.

We sometimes get calls from people who worry that because they’re in debt to their utility provider for their gas and electricity that this is against the terms of their IVA.

This isn’t the case, in fact it’s one of the many myths about IVAs. While being indebted to your utility provider is a form of credit it isn’t against the terms of your IVA as long as you maintain the payments as agreed.

Whilst it may seem like a good idea to borrow from your family or friends they will still need to be paid back and this could affect your ability to make your IVA payments.

Its okay to accept a gift from family or friends but do not take a loan – contact you IVA supervisor instead.

Alongside these debts, another to consider is catalogue debt. People sometimes don’t see a catalogue debt as a real debt because often people in IVAs find that they can get approved for some catalogue transactions.

This is against the terms of your IVA.

While catalogue debts might be small they’re a form of credit which can quickly build up and affect your ability to maintain payments into your IVA.

Needing items from catalogues suggests that your IVA budget might not be working. We’d prefer you call us to discuss your IVA budget before you decide to take on catalogue debt and risk breaching your arrangement. Go back to the quick recap in section 1…

Remember, just say no to payday loans.

If you do have a sudden unexpected expense or bill to pay and you can’t afford it, we’d prefer if you called us (or your IVA provider) to discuss how we can help you through this without relying on further credit.

There’s a risk of bankruptcy if your IVA fails, so we’re here to help you make sure your IVA completes its course. We’re also here to listen to you and help you stick to the terms of your IVA the whole duration of the arrangement.

If you’re tempted to take new credit you should speak to us first, to see if we can arrange an alternative solution which will keep you and your IVA on the straight and narrow.

Responses